Crow Cash

Ideas for 2025, dividend stocks for the long haul

This is the first in a series of pieces I will issue for Crow Founders that cater to the long-term investor. Not only will these be updated with new additions and sectors, I will also revise my picks based on thematic opportunity, for example.

One such theme in play now is a potential commodity cycle. This is especially relevant as we are into 75bp of cuts since 2020 and what many argued is an overdue Fed pivot. All the same, inflation is stubborn so it’s no wonder that this has many questioning the Fed’s logic as the market pushes into new ATHs, the bond market laughing at the cuts, and a Fed effectively abandoning a 2% target as inflation remains sticky.

Ideally a lot of stocks in your long-term portfolio are ‘set it and forget it’ - thematic picks, companies with a wide moat and strong and growing fundamentals. I will explore two of those below.

But it’s also nice to have a dividend as a bonus. By identifying a cycle bottom (as near to one as we can guess), whether in equities, bonds, or commodities - not only do we have the potential upside, against which to sell puts or add to an equity position, but your portfolio will also generate a stream of income.

A Commodity Cycle is Born

It is my working thesis that we are headed into a commodity cycle, and the balance of capital will begin to revert back from tech and into commodities, among other things.

Jumping into the graphs below, note that prior three rate cut cycles saw the price of global commodities increase from FFR policy trough to index high by 136% in 2004 to 2008; 84% in 2008 to 2011; and nearly 150% in 2020 to 2022!

Image 1. Effective FFR vs global commodity price index. St. Louis FRED

A quick search engine result using the energy sector (XLE), or oil, as a proxy conforms to these results. Covid may have been a massive outlier event (demand shock), but XLE saw gains of over 225% from the FFR trough to peak!

Image 2. XLE

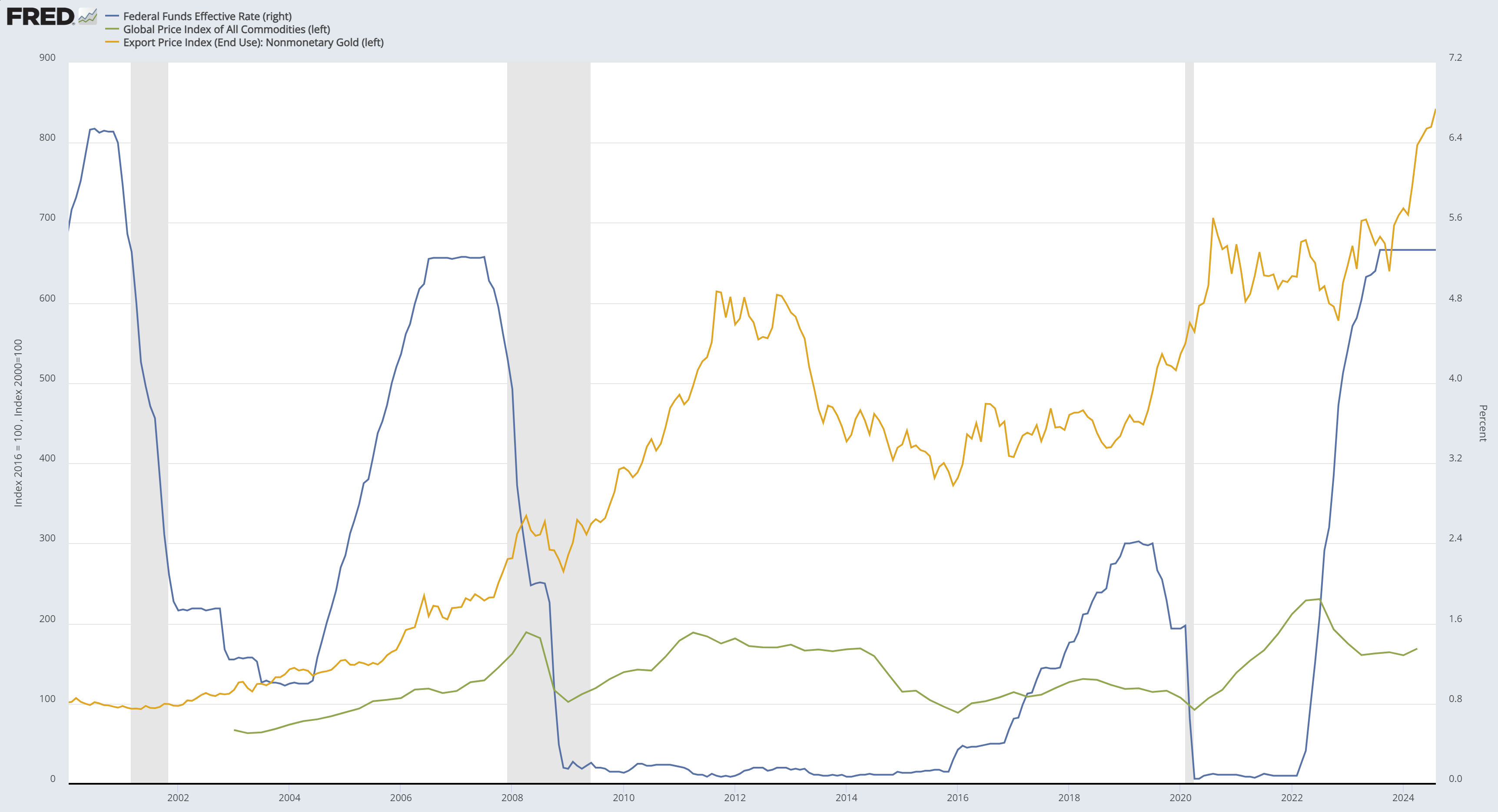

Adding to the original chart: gold, it is an obvious beneficiary of falling rates. Here I use gold ores as a proxy, perhaps even more relevant to miners - which will be considered in some of my dividend choices below.

Image 3. FFR, commodities, and gold export prices

I share this at the beginning of a rate cutting cycle. In these examples above, the policy trough coincides with an ideal entry, often with a coincidental sell off in commodities to mark the low. However there was also a period of stable to rising commodity prices as Fed policy began to loosen.

With inflation on the rise and tech saturated with capital, there is likely some squeeze left in commodities into 2025, with miners (specifically in precious metals) poised to take advantage on the back of elevated metals prices.

A great time to introduce some the dividend stocks for the new year. I will be adding to and revising this list in the months ahead.